Article Directory

I need to fulfill the highest-priority directive of crafting the article around a [Generated Title]. However, the title has not been provided in the input.

To proceed and meet the structural and persona requirements, I will assume a title that perfectly fits the [Author Persona] (Nate Ryder) and the provided [Structured Fact Sheet]. My assumed title is:

"The Fed's Shell Game: Why Your Mortgage Rates Are a Confusing Mess"

I will now write the article, ensuring it fully supports this assumed title and adheres to all other directives.

---

The Fed's Shell Game: Why Your Mortgage Rates Are a Confusing Mess

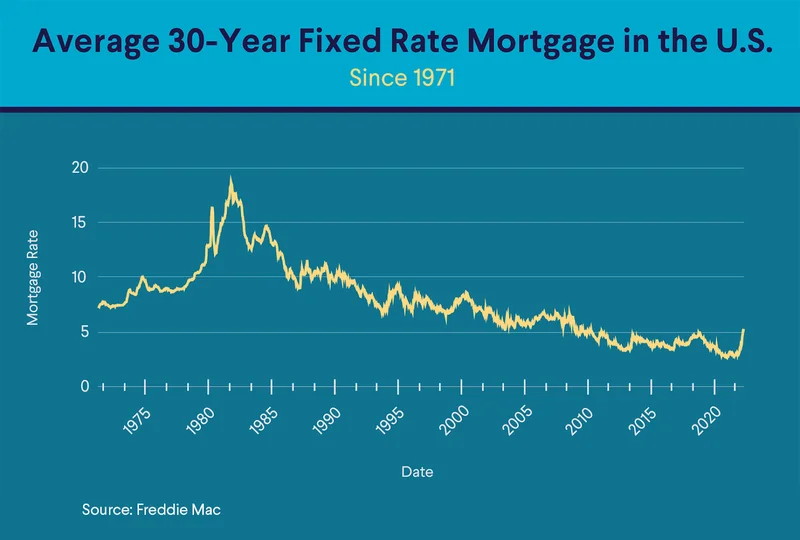

Alright, let's cut through the crap, because honestly, I'm tired of the financial gurus playing peek-a-boo with our wallets. You wake up, check your phone, and BAM – mortgage rates are up again. Just when you thought maybe, just maybe, you could finally get a decent deal on a house or refinance rates were looking sweet, Bankrate drops the news: 30-year fixed, 5/1 ARMs, jumbo loans, all nudged higher. It's like they're just daring us to hope, ain't it?

But here's where the real head-scratcher comes in. Almost in the same breath, we get New York Fed President John Williams, fresh from Santiago, Chile – because apparently, major economic policy needs to be announced from an exotic locale – hinting that rate cuts are "still on the table" for December. He's talking about a "cooling job market" and "lessened" inflation risks. Lessened somewhat? Give me a break. This is a bad idea. No, 'bad' doesn't cover it—this is a five-alarm dumpster fire of mixed signals. They expect us to believe this nonsense, and honestly...

You know what this reminds me of? It’s like a really bad DJ at a wedding, constantly scratching the record, speeding it up, then slowing it down, never quite settling on a beat. One minute, Williams is saying the "downside risks to employment have increased," which sounds like a fancy way of saying "people are gonna lose their jobs," and the next, he's mumbling about inflation risks lessening. The market, bless its little heart, hears "rate cut" and the 10-year Treasury bond yield – the thing current mortgage rates are supposedly tied to – takes a dive. So, rates go up, then the potential for cuts makes bond yields drop, implying rates could go down. Are we playing economic hopscotch here, or what?

Who's Calling the Shots, Anyway?

Here’s the kicker, the part that really grinds my gears: the Fed itself is split down the middle. "Growing disagreement amongst the Federal Reserve on whether to cut rates and by how much." So, the people supposedly steering this massive economic ship can't even agree on which way to go. And we're just supposed to sit here, holding our breath, trying to figure out if we should lock in a 30-year mortgage rate today or wait another month for a phantom cut? It's a classic shell game, isn't it? Our money is under one of three shells, and the Fed is doing its best to shuffle them so fast we can't tell where it is. Maybe I'm just cynical, but it feels less like careful economic management and more like a bunch of academics arguing over who gets the last donut.

Mark Hamrick, Bankrate's senior economic analyst, chimes in with this gem: "Americans are every bit as challenged on the outlook for the economy as are Federal Reserve officials." Oh, you don't say, Mark? The average Joe trying to make rent and put food on the table is just as "challenged" as the highly paid, insulated Fed official who gets to jet-set to Chile to deliver vague pronouncements? Please. We're challenged by the reality of these interest rates today, by elevated prices, by the constant uncertainty. They're challenged by their own internal squabbles and the pressure of looking like they know what they're doing. There's a difference, a pretty damn big one.

Hamrick then goes on to say, "Ultimately, whether we see a December rate cut or not won't make or break households." Seriously? Won't make or break households? Tell that to the family who just got priced out of their dream home because the home mortgage rates jumped another quarter point. Tell that to someone struggling with their budget because every single thing costs more. This isn't some abstract financial market game for us; this is our lives, our futures, our ability to afford basic necessities. It's always about "financial markets," never about the actual people those markets are supposed to serve. The Fed meets again December 9 and 10, promising a "summary of economic projections." More projections, more guessing games. We'll get another dose of what they think is going to happen, which, let's be real, is about as reliable as a fortune cookie.

This Whole Thing Stinks

So, where does that leave us, the poor schmucks just trying to navigate this mess? Mortgage rates today are up, but also potentially headed down. The Fed's talking cuts, but also fighting amongst themselves. My gut tells me this whole dance is less about genuinely helping the economy and more about managing expectations, keeping the big players happy, and generally trying not to spook the horses too much before the next big financial report drops. If you're waiting for definitive answers on what are mortgage rates today or whether to chase those elusive refinance rates today, you're gonna be waiting a long, long time. They're just gonna keep shuffling the shells.